Private Student Loans: A Complete Guide

Welcome to the ultimate guide on private student loans! Whether you’re a high school senior preparing for college or a current student looking for ways to fund your education, navigating the world of student loans can be overwhelming. In this comprehensive guide, we’ll break down everything you need to know about private student loans, from how they work to tips for finding the best one for your financial situation. Let’s dive in and make the process of financing your education a little less stressful!

What are Private Student Loans?

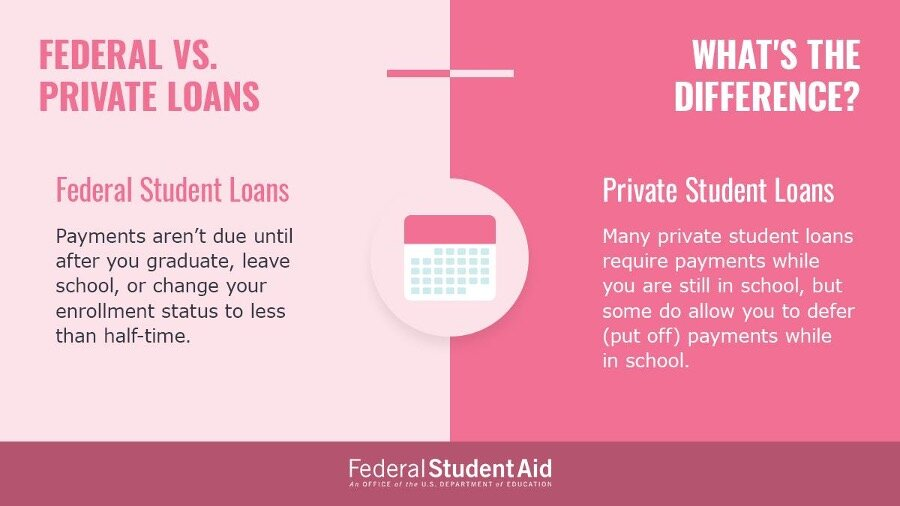

Private student loans are loans that are granted by private financial institutions, such as banks or credit unions, to help students pay for college expenses. Unlike federal student loans, which are funded by the government, private student loans are funded by private lenders. These loans can be used to cover tuition, textbooks, housing, and other education-related costs that may not be fully covered by federal financial aid.

One of the key differences between private student loans and federal student loans is the interest rates. While federal student loans typically have fixed interest rates set by the government, private student loan interest rates can vary depending on the lender, the borrower’s creditworthiness, and other factors. This means that students who have a good credit score may be able to secure a lower interest rate on a private student loan compared to a federal loan.

Private student loans also offer more flexibility in terms of repayment options. While federal student loans have standard repayment plans set by the government, private lenders may offer a variety of repayment plans to meet the individual needs of borrowers. This can include options such as interest-only payments while in school, deferment of payments until after graduation, or even income-based repayment plans.

Another important aspect of private student loans is that they typically require a credit check. This means that students with a limited credit history or poor credit score may need a co-signer, such as a parent or another family member, to qualify for a private loan. Having a co-signer can help increase the likelihood of approval and secure a lower interest rate on the loan.

Overall, private student loans can be a valuable resource for students who need additional funding for their education expenses. However, it is important to carefully consider the terms and conditions of the loan before borrowing. Students should compare interest rates, repayment options, and fees from multiple lenders to ensure they are getting the best deal possible. Additionally, students should only borrow what they need and be mindful of their ability to repay the loan after graduation.

Pros and Cons of Private Student Loans

Private student loans can be a helpful option for students who need additional funds to cover the cost of their education. These loans are offered by private lenders and typically have higher interest rates compared to federal student loans. However, they also come with their own set of pros and cons that students should consider before taking one out.

Pros:

1. Flexibility: Private student loans offer more flexibility in terms of loan amounts and repayment options. Students can borrow the exact amount they need to cover tuition, books, and other expenses without being limited by federal loan caps. Additionally, private lenders often provide multiple repayment plans, allowing students to choose the one that best fits their financial situation.

2. Faster Approval Process: Private student loans generally have a quicker approval process compared to federal loans. This can be beneficial for students who need funds urgently and cannot wait for the longer processing times of federal loans. Some private lenders even offer instant approval decisions, making it easier for students to access the money they need for their education.

3. Potentially Lower Interest Rates: While private student loans typically have higher interest rates than federal loans, some private lenders may offer competitive rates to attract borrowers. Students with good credit scores may be able to secure a lower interest rate on a private loan, potentially saving them money over the life of the loan.

4. No Borrowing Limits: Unlike federal loans, which have annual and lifetime borrowing limits, private student loans do not have strict borrowing limits. This can be beneficial for students attending expensive universities or pursuing advanced degrees that require additional funding beyond federal loan limits.

Cons:

1. Higher Interest Rates: One of the main drawbacks of private student loans is the higher interest rates compared to federal loans. This can result in students paying more over the life of the loan, especially if they borrow a significant amount. It is important for students to carefully consider the interest rate before taking out a private loan.

2. Lack of Federal Benefits: Federal student loans offer various benefits, such as income-driven repayment plans, loan forgiveness programs, and deferment options. Private student loans typically do not offer these benefits, making it harder for students to manage their loan payments in times of financial hardship. It is important for students to understand the differences between federal and private loans before making a decision.

3. Credit Check Required: Most private lenders require a credit check to qualify for a student loan. This can be a barrier for students with limited or poor credit history, as they may not be eligible for a private loan or may be offered higher interest rates. Students should review their credit report and work on improving their credit score before applying for a private loan.

4. Cosigner Requirement: Many private lenders require a cosigner for student loans, especially for undergraduate students or those with limited credit history. Having a cosigner can help students qualify for a loan and secure a lower interest rate, but it also puts the cosigner at risk if the student is unable to make payments. Students should carefully consider the implications of having a cosigner before taking out a private loan.

In conclusion, private student loans can be a valuable resource for students who need additional funding for their education. However, it is important for students to weigh the pros and cons of private loans carefully and consider their individual financial situation before deciding to borrow from a private lender.

How to Apply for Private Student Loans

When it comes to applying for private student loans, there are a few key steps that you need to follow in order to successfully secure the funding you need for your education. Here is a detailed guide on how to apply for private student loans:

1. Research and Compare Loan Options: Before you start the application process, it’s important to research and compare different private student loan options available to you. Look for lenders that offer competitive interest rates, flexible repayment options, and good customer service. Consider factors such as loan limits, interest rates, fees, and repayment terms when comparing loan options.

2. Check Your Eligibility: Once you have narrowed down your list of potential lenders, you will need to check your eligibility for each loan. Most lenders will require borrowers to have a good credit history and a cosigner if they are an undergraduate student. Make sure to review the eligibility requirements for each loan carefully to ensure that you meet all the criteria before applying.

3. Gather Necessary Documents: Before you begin the application process, it’s important to gather all the necessary documents that lenders will require. This may include your Social Security number, driver’s license, proof of income, tax returns, and information about your academic program. Having these documents ready will help streamline the application process and increase your chances of being approved for a private student loan.

4. Fill Out the Application: Once you have all the necessary documents, you can start filling out the application for the private student loan. Most lenders have online applications that you can complete on their website. Make sure to provide accurate information and double-check all the details before submitting your application to avoid any delays in the approval process.

5. Review and Compare Loan Offers: After submitting your application, you may receive offers from multiple lenders. Take the time to carefully review and compare the loan offers you receive, paying attention to the interest rates, fees, and repayment terms. Consider reaching out to the lenders directly if you have any questions or need more information about the terms of the loan.

6. Accept the Loan Offer: Once you have chosen a loan offer that best suits your needs, you can accept the offer and proceed with the loan disbursement process. Make sure to carefully review the loan agreement and terms and conditions before accepting the offer to ensure that you understand all the obligations associated with the loan.

7. Disbursement of Funds: After accepting the loan offer, the lender will disburse the funds directly to your school to cover the cost of tuition, fees, and other education-related expenses. Make sure to follow up with your school’s financial aid office to ensure that the funds are applied to your student account in a timely manner.

By following these steps, you can successfully apply for a private student loan and secure the funding you need to pursue your education goals. Remember to stay organized, research your options thoroughly, and communicate with your lender throughout the application process to ensure a smooth and efficient experience.

Private Student Loan Interest Rates

When it comes to private student loans, interest rates play a crucial role in determining the overall cost of borrowing. Unlike federal student loans, which have fixed interest rates set by the government, private student loan interest rates vary depending on factors such as the borrower’s creditworthiness, the lender’s policies, and the current market conditions.

Private student loan interest rates can be either fixed or variable. Fixed interest rates remain the same for the entire loan term, providing borrowers with predictability and stability in their monthly payments. On the other hand, variable interest rates may fluctuate periodically, depending on changes in a predetermined financial index. While variable rates have the potential to be lower initially, they also come with the risk of increasing over time, leading to higher overall costs.

When applying for a private student loan, lenders typically assess the borrower’s credit history and score to determine the interest rate offered. Those with excellent credit scores may qualify for lower interest rates, making borrowing more affordable. Conversely, borrowers with less-than-perfect credit may face higher interest rates, reflecting the increased risk for the lender.

It’s essential for borrowers to shop around and compare offers from multiple lenders to find the best interest rate available to them. Some lenders may also offer discounts on interest rates for factors such as setting up automatic payments or completing a certain number of on-time payments.

In addition to the interest rate itself, borrowers should also consider the impact of fees on the overall cost of the loan. Some lenders may charge origination fees, application fees, or prepayment penalties, which can add to the total amount repaid over the life of the loan. Understanding all the potential costs associated with the loan is crucial in making an informed decision on which private student loan to choose.

It’s also worth noting that refinancing student loans can be an option for borrowers looking to lower their interest rates or monthly payments. By refinancing with a new lender, borrowers may qualify for a lower interest rate based on their current financial situation and creditworthiness. However, borrowers should carefully weigh the benefits of refinancing against any potential drawbacks, such as losing access to federal loan benefits or deferment options.

In conclusion, private student loan interest rates are a significant factor to consider when borrowing money for education. By understanding how interest rates are determined, comparing offers from multiple lenders, and considering the impact of fees, borrowers can make informed decisions that minimize the cost of borrowing and save money over time.

Repayment Options for Private Student Loans

When it comes to repaying private student loans, borrowers have a few different options available to them. The repayment options for private student loans can vary depending on the lender, but generally include options such as standard repayment, extended repayment, graduated repayment, income-based repayment, and deferment or forbearance.

1. Standard Repayment: This is the most common repayment option for private student loans. With standard repayment, borrowers make fixed monthly payments over a set period of time, usually around 10 years. This option typically results in the lowest total repayment amount, but can also lead to higher monthly payments.

2. Extended Repayment: Extended repayment allows borrowers to extend the repayment period beyond the standard 10 years, usually up to 15, 20, or even 25 years. This can result in lower monthly payments, but borrowers will end up paying more in interest over the life of the loan.

3. Graduated Repayment: Graduated repayment starts with lower monthly payments that gradually increase over time, typically every two years. This option is ideal for borrowers who expect their income to increase in the future but may struggle to make higher payments initially.

4. Income-Based Repayment: Income-based repayment plans adjust the monthly payment amount based on the borrower’s income and family size. These plans can provide relief for borrowers who are struggling to make their payments, but may result in paying more interest over the life of the loan.

5. Deferment or Forbearance: Deferment and forbearance options allow borrowers to temporarily pause or reduce their monthly payments in case of financial hardship or other circumstances. During deferment, interest may not accrue on subsidized loans, but will continue to accrue on unsubsidized loans. Forbearance, on the other hand, allows borrowers to temporarily stop making payments or reduce the amount due, but interest will continue to accrue on all types of loans.

It’s important for borrowers to carefully consider their options and choose the repayment plan that best fits their financial situation. Borrowers should also be aware that private student loans typically do not offer the same flexible repayment options as federal student loans, so it’s crucial to communicate with the lender if experiencing difficulties in making payments. By understanding the different repayment options available, borrowers can effectively manage their private student loan debt and avoid defaulting on their loans.